NVPERS leadership discounts member complaints

Is a very simple error — looking only at one side of the balance sheet — the source of a huge and growing rift between Nevada’s largest teachers union and the Public Employees’ Retirement System of Nevada (NVPERS)?

On the popular TV show, Shark Tank, it’s a virtual certainty that if a presenter boasts about his firm’s sales or revenue, at least one “shark” will immediately ask for the expenses during the same accounting period.

That’s because each of those two data points is only one-half the information needed to assess the health of a business. Relying on one without the other would be incomplete at best, and dangerously misleading at worst.

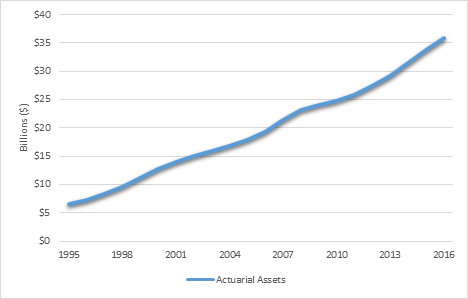

The chart below, or one similar to it, is highlighted every year in NVPERS annual financial report. Updates are presented to the Retirement Board every quarter, and it is routinely referenced at board meetings as evidence of the System’s strong performance:

Chart 1: Growth of NVPERS fund, 1995-2016

Turning $6.5 billion into $35 billion over 20 years is a remarkable feat.

But this information reveals literally nothing about whether or not the System’s primary objective — fully funding the cost of retirees’ promised benefits — is being met.

Thus, attempting to evaluate the System’s performance without also including those costs is like valuing a business on gross revenues while ignoring expenses.

In other words, you’d be flying blind.

What’s worse, the asset-only chart erroneously suggests that NVPERS has never been in better shape.

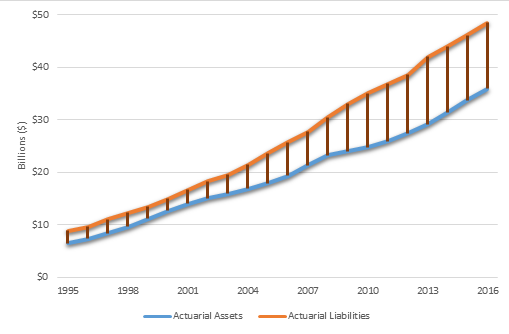

Complete information, however, shows that the exact opposite is true:

Chart 2: NVPERS fund and liabilities, 1995-2016

Counting both sides of the balance sheet reveals that the debt held by the System — the gap between the cost of retirees’ promised benefits (liabilities) and the assets needed to fund them — has soared from $2.2 billion in 1995 to $12.56 billion today.

This debt explosion explains why public workers’ retirement costs have risen to record-high levels — with the 14 percent salary deduction paid by Nevada teachers tied for the highest rate nationwide.

That’s according to NASRA, a public pension research organization run by former NVPERS executive officer Dana Bilyeu.

But nothing like the above chart has ever followed the assets-only chart routinely displayed at board meetings. In fact, a records request for any document in the possession of NVPERS that displayed assets alongside liabilities came up empty.

Such an inordinate emphasis on investment returns is what most likely blinded the Retirement Board to the System’s soaring debt and the consequent burden that debt has imposed on members.

Nowhere was this clearer than at a board meeting from March of this year.

Just minutes after citing the data depicted in chart #1 as evidence of the System’s strong performance, investment consultant Ken Lambert turned the discussion to complaints coming from members of the Nevada State Education Association (NSEA) over their rising contribution rates.

Lambert was then interrupted by NVPERS Board Chairman Mark Vincent, who dismissed the complaints as meritless, believing that the true culprit lied elsewhere:

I feel like it’s more complicated than that…I don’t remember in my professional career having such a vociferous attack on public pensions as we’ve seen in the last decade. My theory is the teachers are idiots, for the most part. They’re math-challenged. They don’t get any of this. It’s the pounding of the attack on public pensions that’s got them stirred up, because they really don’t understand what’s going on…Part of the problem is, I think, the other side is winning. Because they’re grumpy and it feels like, sometimes, that’s all that they are hearing…I don’t think our members understand this stuff at all! Not at all! Not at all!

But the key to understanding members’ complaints can be found within the System’s own governing documents, which the Retirement Board itself adopted.

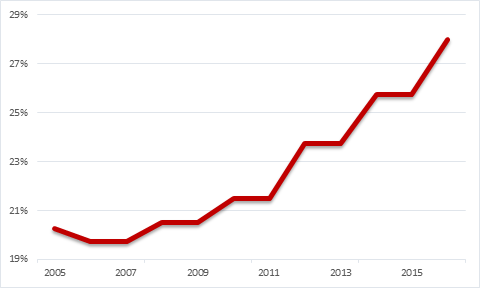

After fully funding retirees’ promised benefits, the second goal listed in NVPERS Actuarial Funding Policy is to ensure that costs are spread in a fair and equitable manner.

Thus, the 40 percent increase in members’ retirement costs over the past decade — all of which went towards previously accumulated debt, not the future benefit of the employee paying them — represents a spectacular failure of this goal.

Chart # 3: NVPERS costs as a percentage of members’ salary, 2005-2016

Rather than stemming from ignorance or external factors, members’ complaints reflect the simple — albeit largely ignored — fact that the System is failing them, as measured by the Retirement Board’s own terms.

While NSEA members may have never seen these charts, they felt them.

Perhaps if complete information was presented on a more regular basis, they would have found a more receptive ear at the Retirement Board.

Further Reading: