News organizations need to stop misleading the public about PERS

A pernicious myth is being spread by some of Nevada’s news organizations about the financial health of PERS — erroneously suggesting the public should be unconcerned about a multi-billion dollar debt that continues to consume more and more tax dollars every year.

Geoff Dornan of the Nevada Appeal made this error again just last month, when he described the System’s unfunded liability as: “…the shortfall PERS would face if the system was dissolved and it had to pay retirement to every covered public employee.”

Likewise, the Nevada Independent falsely claimed in their “The Indy Explains” feature that PERS unfunded liability represents the amount that would have to be paid if the “government were to stop all operations at once and need[ed] to settle current and future debts to all PERS participants immediately.”

The Independent went on to say that “because that situation is unrealistic…there’s a range of opinions on how concerned Nevada should be about its unfunded liability.”

Just for the record, if the unfunded liability was an amount that only came due in the event the government ceased to exist, it would be worth ignoring.

However, that’s not at all what PERS unfunded liability represents.

In fact, neither news organization can cite any actuary or even any PERS official as a source for this false definition. The Independent acknowledged as such when alerted to their error by the Nevada Policy Research Institute, and agreed to seek out an accurate definition.

Unfortunately, it has so far failed to publish a correction or update the feature, which was written in February of 2017.

So what is the correct definition?

As a first step, we have to understand how a pension fund calculates its liabilities. Here’s a simplified example to illustrate the concept:

Say PERS had to make a $20 payment ten years from now, but currently has only $10 on hand. At first glance, it would seem like the System is only 50 percent funded, and would report a $10 unfunded liability. In practice, however, PERS reduces its reported liability by the amount it expects to gain from assumed future investment returns.

So, if the System posits that its future investment returns will boost its current $10 worth of assets to $20 over the next ten years, it would report a 100 percent funded ratio with no unfunded liability — as it expects to have all of the money owed by the time the payment is due.

Conversely, if the System only had $5 on hand, it would not expect to be able to meet its future obligation of a $20 payment in ten years from investment gains. It would then report an unfunded liability of five dollars, representing the additional amount the system needs immediately in order to be able to earn enough from investments over the next decade to make the $20 payment.

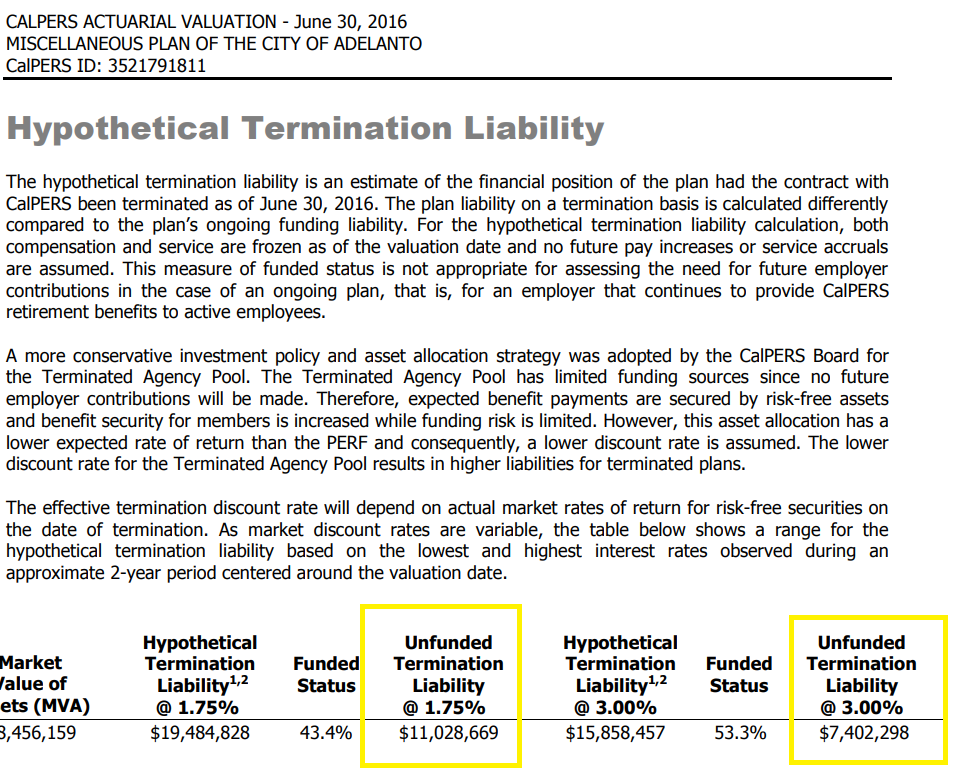

To get a sense of the magnitude of difference between the reported unfunded liability and the amount that would be owed in a termination event we can consult the nation’s largest public pension fund, The California Public Employees’ Retirement System (CalPERS) — which reports both the regular unfunded liability and the unfunded termination liability.

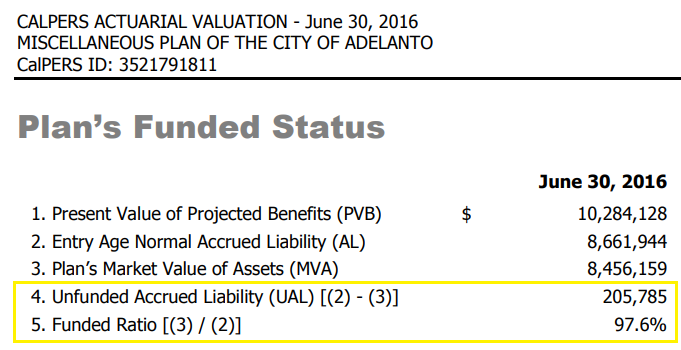

The California city of Adelanto, for example, currently enjoys a funded ratio of 98 percent and a tiny unfunded liability of only $205,000.

{kind=link}

Yet, if Adelanto were to terminate its pension plan and had to fund all promised benefits today, its unfunded liability would explode from a mere $205,000 to as much as $11 million!

{kind=link}

As this example illustrates, PERS unfunded liability is just a small fraction of the amount that would be owed if the System had to pay out all of its already-promised benefits immediately.

This principle is an uncontroversial and universally recognized fact, making the continued repetition of this gaffe so perplexing. (See, for example, the New York Times article “A Sour Surprise for Public Pensions: Two Sets of Books”).

So now we can identify what the unfunded liability actually represents: It’s a shortfall above and beyond what PERS expects to make from future investment returns. And therefore it’s an amount that instead must be paid entirely by taxpayers and government workers.

With this definition in mind, it becomes clear why, beyond the importance of simple accuracy, misrepresenting PERS $13 billion unfunded liability as an abstract, meaningless figure is so harmful.

To its credit, PERS recognizes the importance of eliminating its unfunded liability and, as such, currently expects to pay it off over the next 19 years or so. But the repeated misrepresentation of this figure obscures how PERS plans to pay that debt down — solely by raising taxpayer and public worker contributions!

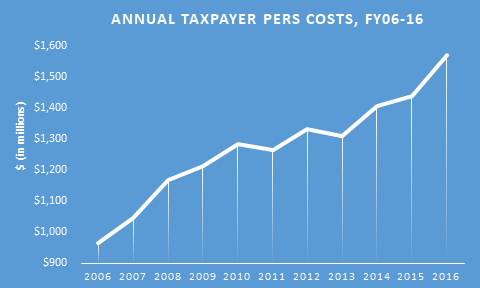

In fact, this is precisely why taxpayer contributions to PERS hit an all-time high of $1.57 billion last year — an amount which ranked 2nd-highest nationwide when measured as a percentage of government revenue. It’s also why those contributions are set to rise even further in coming years, forcing cuts in public services, higher taxes or a combination of the two.

Already the amount docked from teachers’ paychecks to help fund PERS has risen 40 percent over the past ten years, leaving teachers paying some of the highest rates in the nation, without any corresponding increase in benefits.

Yet these real-world costs are regularly neglected in most news coverage of PERS, and not just in smaller newspapers like the Nevada Appeal.

Even former Review-Journal reporter Sean Whaley — who has since been hired by PERS as an independent contractor to help with their communications efforts — has downplayed or simply omitted taxpayer costs in his periodic updates on the fund’s growth. (See, for example, here, here and here.)

Such omissions are serious, given that these costs, and the burden they impose on the taxpayers and public employees who must pay them, are the only reason PERS warrants media coverage in the first place!

And it’s not like there hasn’t been anything to report on in this regard:

(Click here to see these costs adjusted for both inflation and membership growth,

and here as a percentage of payroll.)

The continued rise in PERS costs is already leaving fewer tax dollars available for public safety, road repair, teacher salaries and other public services — making PERS one of the state’s most important public policy issues, despite being one of the least understood.

As such, it is imperative that news organizations remember why they are reporting on PERS in the first place, and provide the public with complete and accurate information.

One of the best examples of comprehensive public pension reporting is the extensive, multi-part series on California’s public pensions recently published by the Los Angeles Times. It is a fantastic resource for any journalist or member of the public wishing to get more familiar with the topic.

Robert Fellner is NPRI’s policy director. To read more from NPRI about Nevada PERS, click here.